Agroforestry's 2.0 Moment

Our work is noble, but the industry needs to better speak the language of investors while meeting their needs and desires over time.

1. Headline

As a practice, agroforestry is incredibly powerful in its ability to rehabilitate soils, stop erosion, improve water quality, return biodiversity to agricultural landscapes, sequester carbon, and bolster rural economies. That said, publicly available data suggests that only a small portion of all nature-based solutions (NbS) investing finds its way to agroforestry projects, at present. We firmly believe that this dynamic will change in the years ahead, however we are also sober about the actions and language that will be required from agroforestry practitioners to enable more capital into the space. As we explain in the report ahead, we think there is much to be gained by focusing on products relative to practices; further de-risking operations; and fine-tuning the plumbing mechanisms around underlying agroforestry projects.

2. What does this mean?

On any given day, Agroforestry Partners speaks with investors and corporate funders that span a wide spectrum of impact areas and asset classes as we continue our fundraising efforts to advance agroforestry in the United States. From these conversations, we’ve realized two main realities about our industry’s position in the marketplace:

Agroforestry is powerful, but it is also comparatively complex and unique.

A new evolutionary approach is needed if we want to scale this important work.

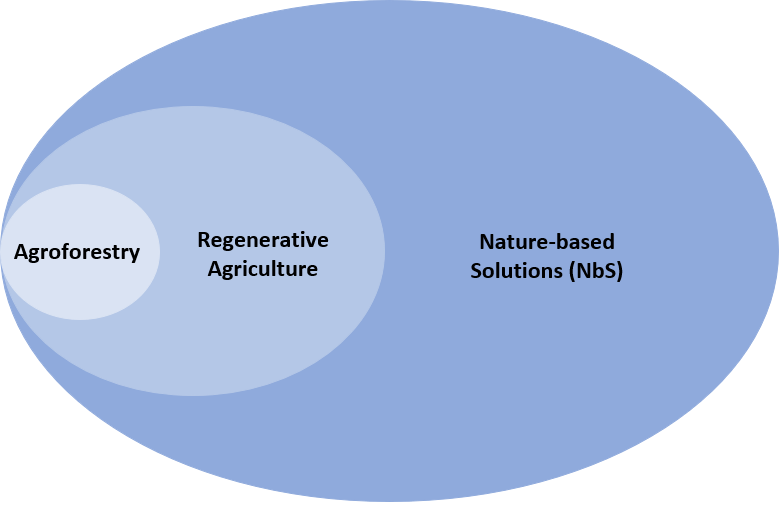

First, we must acknowledge that the practice of agroforestry is nested within the regenerative agriculture movement, the latter of which is itself nested inside the realm of nature-based solutions (NbS). We might also add, as well, that NbS is many times considered as a subset of climate investing more broadly. As agroforestry project developers and managers, we all need to keep this in mind and tailor our message, accordingly. To be sure, a regenerative agriculture investor will have different wants and needs relative to a NbS or climate investor. All of them are evaluating agroforestry against many other options across the NbS/climate space writ large.

According to the United Nations Environment Program’s (UNEP) 2026 State of Finance for Nature report, total private finance flows into NbS measured $23.4 billion globally in 2023 (public expenditures on nature were $197 billion). A vast majority of this private financing allocated to nature came from corporate payment for nature/carbon offsets, corporate green bond issuances, and corporate payment for certified commodity supply chains (think sustainable timber or fisheries). Thus, companies have been a big driver of private-sector nature spending thus far.

What about investment funds? Risk-seeking investment funds allocated $1 billion towards NbS pursuits in 2023 while philanthropic funders channeled around $271 million. We don’t have good data for how risk-seeking funds allocate their capital, however philanthropic data likely provides a good analogue for the total overall. On this basis, just over 25% of funding goes to regenerative agriculture while the vast remainder is applied towards “biodiversity” (this is a wide catch-all that includes everything from habitat protection to forest preservation to marine health safeguards). In the UNEP report, agroforestry did not register as a meaningful sub-group within regenerative agriculture spending, speaking to its current place as a niche conservation approach. Instead, most regenerative agriculture allocations have heretofore gone towards incremental actions that make existing crop and livestock production/products more sustainable. We have written about this dynamic here and here previously, noting that agroforestry remains a comparatively expensive endeavor and that cover crops — in particular — have become a preferred conservation approach for regenerative agriculture advocates in the U.S., as a result. Globally, farm surveys like a recent example out of Brazil consistently show agroforestry as being underappreciated and, therefore, underinvested.

Based on the above information, how can agroforestry stakeholders better navigate the finance landscape and garner a larger proportion of NbS funding, ahead? We lay out our key beliefs below as a call to action for the sector.

As further foundation for this discussion, we should also acknowledge that investors generally like to invest behind income streams that have the potential to grow over time. This is why a large chunk of funding consistently gets devoted to products relative to practices. Corporates are no different. This is the same reason that ag-chem companies devote new capital to biopesticides (as opposed to nature interventions), creating a new product that can grow incremental income over time (why invest behind a one-time practice as a solution when you can create products that require repeat purchases each and every year?). To be sure, early-stage (VC) food sector impact investing follows a similar pattern, as showcased by weekly funding updates from FoodHack (high-protein, low-calorie ice cream!). In a seemingly products-over-practices world, how might agroforestry compete for scarce funding dollars? How might practitioners access corporate capital, as well?

Here’s how we think the agroforestry space can better compete in the capital markets while driving scale on the ground.

» Create Income Growth Profiles Centered on Products

Plant and grow valuable products…and find dedicated offtake.

As a practice, agroforestry is one of the best actions that society can take to rehabilitate soils, stop erosion, improve water quality, return biodiversity to agricultural landscapes, sequester carbon, and bolster rural economies. This dynamic, alone, will act as a pull for capital interest. However, formal capital allocation decisions will only occur if the physical product outputs from these practices are — or can be — formulated into desirable, growing revenue streams. Agroforestry practitioners must work hand in hand with potential corporate buyers to find dedicated offtake programs for these products. This will unlock investor and corporate capital alike.

Stack diversified project offerings.

No matter a producer’s best laid plans, income streams from agroforestry projects will be variable just like any other agricultural endeavor. In order to deliver attractive income profiles to investors over time, agroforestry practitioners must stack diversified project offerings in their portfolio of options to capital providers, providing staggered growth profiles that account for individual project volatility while delivering annual income growth across the whole of the project set.

» Reduce Risk

Pursue incremental change.

Capital allocators remember their mistakes. And they are loathe to repeat them. One of the worst errors that agroforestry developers can make is to move too quickly on too much complexity on the ground. Complexity is (ultimately) great for nature systems. It is terrible for the buildout of a nascent industry (it also tends to push investors towards simpler project options elsewhere). If we as a movement want to guard against taking one step forward followed by two steps backwards, we must pursue projects that deliver incremental change in order to attract capital, verify management approaches, and secure initial financial returns for investors. Otherwise, overconfidence might turn into financial losses that drive investors away from the space for decades to come.

Create insurance mechanisms.

One of the key reasons that massive amounts of capital flow to industries surrounding row crops like corn relates to federally subsidized crop insurance programs that de-risk the production of these commodities. Crop insurance is engrained in the psyches of farmers. It is a security blanket that they cannot do without. For agroforestry developers, many of our present systems and preferred products do not have federal crop insurance coverage in place. It is therefore on us to develop private-sector safeguards that allow investors and corporates (and farmers!) to say yes to a new agroforestry project, protecting their scarce capital that can be allocated to other regenerative agriculture projects with existing insurance coverages.

Reduce costs.

The marginal cost of production is an important factor in any industry — but this is especially true in new, developing industries like agroforestry. As more capital comes into the space, an expanded level of specialty crop production has the potential to create price dislocations in the marketplace. Likewise, there is no doubt that the cost of production for an agroforestry system is currently much higher than other regenerative agriculture pursuits that can be implemented on-farm (it’s important to note here that we believe the return profiles and resulting permanence of agroforestry are well above other substitutes in the marketplace, as well). Thus, agroforestry practitioners must be ruthless in driving down our cost structures in order to make sure that we are delivering ongoing economies of scale while being able to fortify project returns for investors.

» Enable Investment into Practices

Improve organizational structures.

Financial returns associated with agroforestry are very attractive — especially when compared to other NbS solutions involving the protection or restoration of nature. However, the timelines required for agroforestry to deliver these returns span multiple decades owing to tree maturation cycles — far longer than most investors can accommodate. Thus, agroforestry practitioners must deliver organizational and ownership structures that allow investors to fund this work on their preferred timelines (7-12 years) while dually enabling these longer-dated agroforestry projects themselves to flourish.

Work to advance plant genetics.

Conventional ag commodities (and many adjacent regenerative practices associated with these commodities) benefit from long-standing research and development on improved varieties that deliver protection against common pest, disease, and climatic pressures inherent in farming outdoors. For those of us wishing to advance agroforestry practices that rely on specialty crops and systems, we must partner effectively with civil sector actors and other stakeholders to advance genetics for these crops such that improved varieties can deliver quicker timelines to production along with better protection against agricultural production risks.

Establish demonstration projects.

Most investors and corporate capital allocators want to see track records before making investment decisions. This is difficult to deliver within the nascent agroforestry space, at present — especially in mature but vital markets like the United States. Smaller demonstration projects can help to showcase proof of concept while adding confidence that capital deployment into scaled projects can be successful, especially when paired with movement on aforementioned actions named above.

For investors and corporate entities that are sincere in their desire to drive ecological and social impact across society, we cannot stress enough that the inherent beauty and value of agroforestry is, in fact, its permanence. Agroforestry is a long-term commitment, and it is for this reason that the planting of trees on agricultural landscapes is one of the best things that farmers and landowners can do for the land and our planet. But we as an industry need to make it easier to start and fund these projects. This means talking in terms of products, showcasing future income/value growth, reducing risk, and enabling investment. Thereafter, practices on the ground will do the heavy lifting to deliver the impact that society needs today.

3. Key takeaway

Investment money is increasingly flowing into nature-based solutions (NbS) around the world. A good chunk of this capital has thus far come from corporate entities investing behind carbon & biodiversity credits, green bonds, and sustainable supply chains, but investment funds have also been devoting money into areas like nature and regenerative agriculture, as well. If those of us involved in agroforestry want to see more investment dollars come our way, we need to meet capital allocators where they are today by creating income growth profiles that are built on products as opposed to practices, while also continually finding ways to further de-risk our projects. Perhaps most important, agroforestry practitioners need to get creative with our organizational and ownership structures in order to enable investment into long-dated tree systems that also meet shorter inherent timelines required by funders.

4. Where to find us

Check us out on our homepage or come connect with us on LinkedIn.

We’re an investment fund that raises money from long-term investors to pay farmers and landowners to plant trees on their properties alongside crops and/or animals, returning nutrients to the soil and our food while delivering attractive, uncorrelated returns to investors.

I am working on an article as to how I wanted to do these things slightly differently than most.

One of my big ideas was plant mostly by seed, for genetics. I also have a “specimen tree” thornless honey locust, which I intend to neopolyploidize to create a tetraploid honey locust so it will be permanently thornless, unable to cross with wild thorned versions, and then create a seedless triploid, for planting in grazing pastures, so cattle can eat it but not make forests.

And also bois d’arc, but I wanted to mechanize silk production, and utilize daisuigi to that end. Then use bodark and honey locust to afforest the American West.

Another thing is Castanea ozarkensis…